On September 29, India's Ministry of Commerce and Industry and the Directorate General of Trade Remedies announced the final ruling in the anti-dumping investigation concerning solar cells and modules from China, proposing to impose anti-dumping duties on solar cells and modules originating in or imported from China for a period of three years. The DGTR's final ruling (signed on September 30, 2025) has recommended implementation "from the date of notification" and specified three tiers of duty rates: 0%, 23%, and 30%, valid for three years. According to India's anti-dumping procedural practices, the CBIC typically completes the notification and publishes it in the Gazette of India, Extraordinary, within 30 days after the final ruling.

In 2024, multiple Indian PV enterprises, including FS India Solar Ventures, Jupiter International, Tata Power Solar, and TP Solar, filed an application with the Directorate General of Trade Remedies (DGTR) of India, alleging that solar cells and modules imported from China were being sold at low prices, causing significant harm to the domestic industry. On September 30, 2024, DGTR issued a notice in the Gazette of India formally initiating an anti-dumping investigation into solar cells and modules imported from China. The notice was also delivered to the Embassy of China in India, relevant Chinese exporters, Indian importers, and end-users, requesting the submission of comments and questionnaires. During this period, questionnaires were distributed to 118 Chinese enterprises, with 74 responding. The period of investigation (POI) spanned from April 1, 2023, to March 31, 2024, with comparative data retrospectively analyzed for the period from 2020–21 to 2022–23.

In 2024, multiple Indian PV enterprises (including FS India Solar Ventures, Jupiter International, Tata Power Solar, TP Solar, etc.) filed an application with the Directorate General of Trade Remedies (DGTR) of India, claiming that imported solar cells and modules from China were being sold at low prices, causing serious harm to the domestic industry. On September 30, 2024, DGTR issued a notice in the Gazette of India, formally initiating an anti-dumping investigation into solar cells and modules imported from China. The notice was also delivered to the Chinese Embassy in India, relevant Chinese exporters, Indian importers, and end-users, requiring them to submit comments and questionnaires. During this period, questionnaires were sent to 118 Chinese enterprises, with 74 responding. The period of investigation (POI) was from April 1, 2023, to March 31, 2024, with comparative data reviewed retrospectively from 2020–21 to 2022–23.

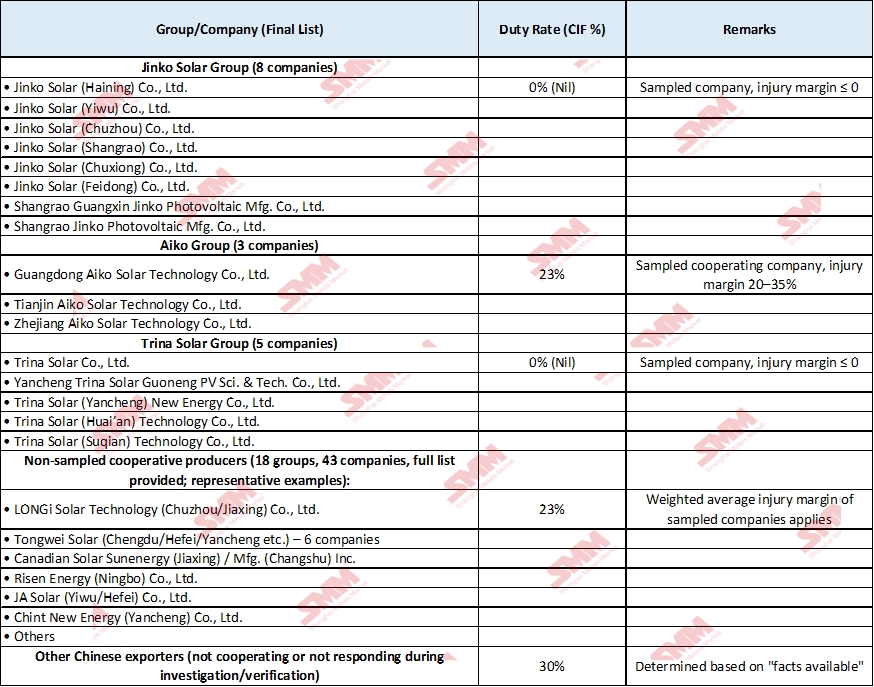

DGTR distributed investigation questionnaires to major Chinese PV exporters (such as Jinko, TrinaSolar, LONGi, AIKO, etc.) to collect information on costs, export prices, and other relevant data.

Various parties, including Chinese exporters, Indian importers, industry associations, and user enterprises, submitted their comments. Chinese enterprises largely argued that no dumping had occurred or contended that imposing additional tariffs would increase the cost of PV systems in India and hinder the development of renewable energy. Indian industry representatives, however, asserted that Chinese enterprises had large-scale surplus capacity and were exporting at prices below cost, severely impacting new capacity investments in India. They warned that without measures, domestic investments (including large-scale expansion projects under the PLI incentive scheme) would face losses or even shutdowns.

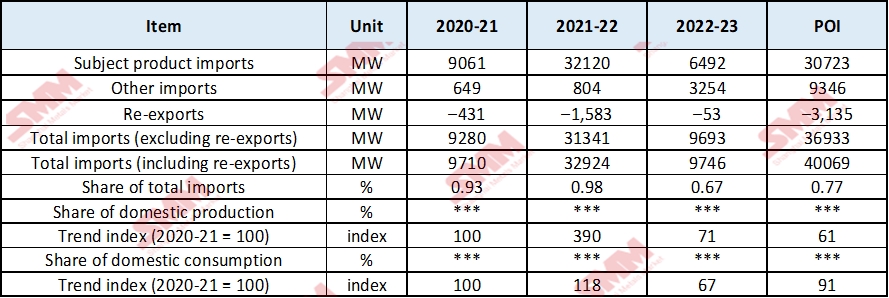

On September 21, 2025, DGTR issued a disclosure statement, making key facts public and soliciting final comments. On September 29, it released the final determination, concluding that Chinese enterprises had engaged in dumping and caused material injury to the Indian industry. The decision recommended the imposition of anti-dumping duties, with varying rates applicable to different enterprises. Both cells and modules were included within the scope of the investigation, rejecting the argument that "cells and modules are independent products" on the grounds that cells must be assembled into modules to be usable, and that both TOPCON cells and thin-film modules share the same end-use as like products, with exclusions potentially leading to tariff evasion. Indian authorities stated that during the investigation period, imports of Chinese products reached 30,723 MW, accounting for 77% of India's total imports, up 373% YoY compared to the previous period (April 2022–March 2023) and an increase of 240% from 2020–21.

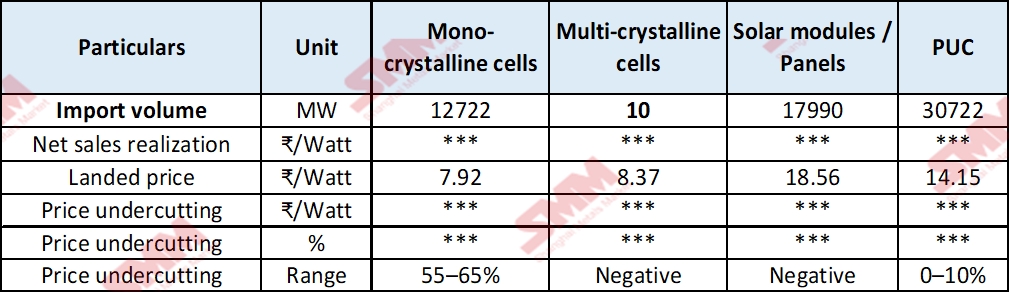

The final ruling determined that the import price of monocrystalline silicon cells was only 7.92 rupees/W (approximately 0.63 yuan/W), with a price reduction margin of 55–65%, while the price of PV modules was 18.56 rupees/W (approximately 1.49 yuan/W), with no price reduction.

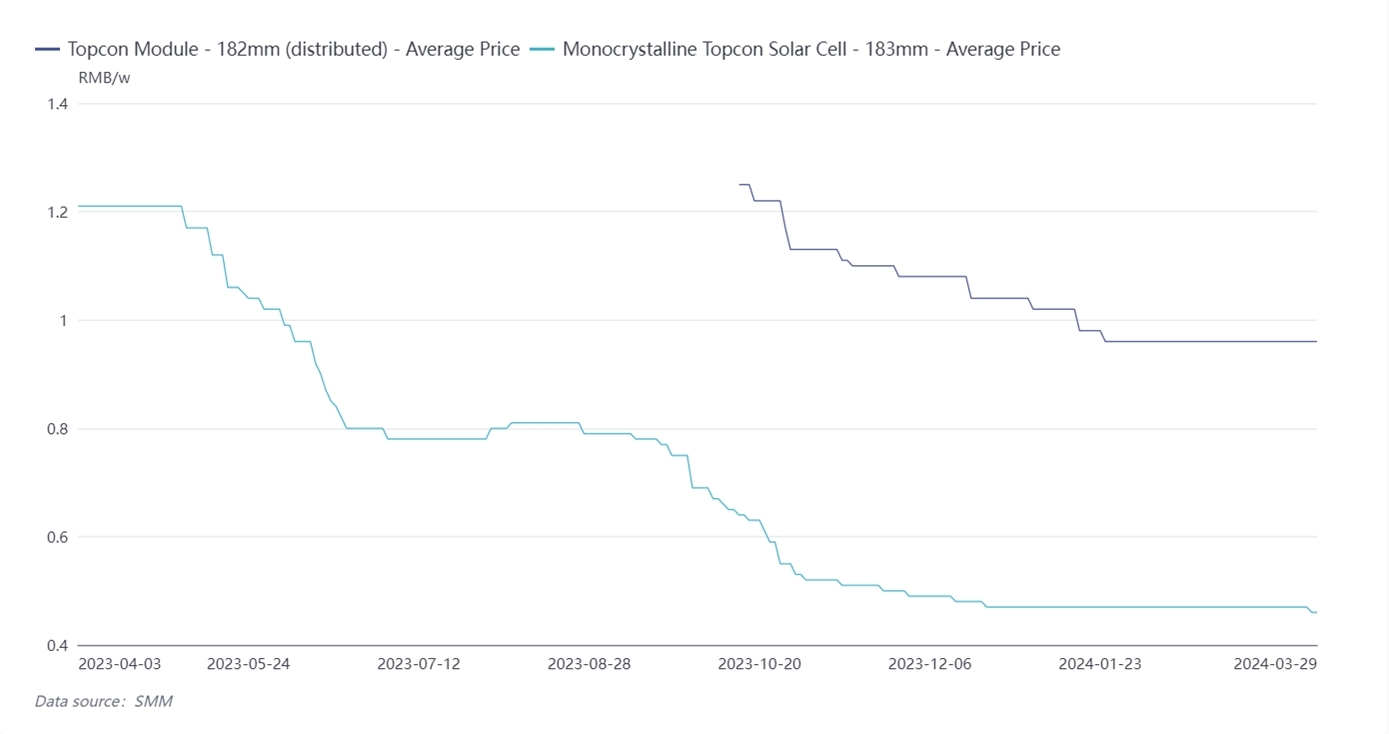

In comparison, in March 2024, SMM reported the average price of "monocrystalline Topcon solar cell-183mm" at 0.47 yuan/W and the average price of "Topcon module-182mm (distributed)" at 0.96 yuan/W.

Indian authorities stated in the report that China's low-price dumping of solar cells and PV modules directly led to a 289% decline in the domestic industry's profitability during the injury period, with profits falling by 184% and cash flow decreasing by 169%. Inventory levels of the local industry surged 68-fold, accompanied by significant losses in related contracts.

Regarding the potential supply-demand gap caused by price increases of solar cells and modules after the imposition of anti-dumping duties, Indian authorities indicated in the final ruling that investigation evidence showed India's solar industry had secured 38.1 GW of new capacity by the end of 2025, with further expansion to 64.6 GW expected by June 2026 (§176), sufficient to meet the annual new demand of approximately 44 GW during the same period, achieving a self-sufficiency rate of over 140% and thereby eliminating any potential supply-demand gap after the tariff imposition. Meanwhile, disclosed projects alone involve nearly ₹1 trillion in capital expenditure, with asset security identified as a core statutory objective to "ensure the feasibility of subsequent investments." In contrast, China, facing successive closures of major export channels by the US (anti-dumping and countervailing duties + Section 201 safeguard duties + 50% surtax), Turkey (anti-dumping duties extended to transshipments from Southeast Asia), Canada (anti-dumping and countervailing duties), and the EU (anti-circumvention investigations), has idle solar capacity as high as 252 GW, equivalent to 576% of India's total demand. The final ruling concluded that against the backdrop of "almost all major global markets imposing restrictions," there is an urgent risk of this massive surplus capacity being redirected to India, which would inevitably exert dual pressure on local new capacity through price suppression and volume impact, thereby endangering the safety of approximately ₹1 trillion in investments already made. Therefore, imposing anti-dumping duties was deemed a "necessary and minimal" relief measure to safeguard industry survival, ensure investment recovery, and achieve supply-demand balance.

In terms of the final tariff imposition outcome, India applied varying degrees of tariffs to different enterprises. The final ruling implemented a "group & individual enterprise" two-tier tariff system for Chinese exporters, with two additional tiers for non-sampled but cooperating enterprises and non-cooperating enterprises, resulting in three tiers: 0%, 23%, and 30%. All tariffs are levied based on CIF value, valid for three years, which is shorter than the typical five-year duration for anti-dumping duties.

Notes:

- Enterprises within the same group enjoy the same tax rate and do not require further subdivision.

- If an exporter ships goods through a third-party trading company, the group tax rate still applies as long as the producer belongs to the aforementioned group.

- For goods not of Chinese origin but transshipped through China, if non-Chinese origin cannot be proven, the 30% rate also applies.

Overall, India’s imposition of anti-dumping duties on China exhibits three characteristics: the duty rate is relatively small, the duty period is relatively short, and a differentiated duty approach has been adopted. SMM analysis suggests the reasons may include the following:

1. Both Article 17(4) of India’s Anti-Dumping Rules and Article 9.1 of the WTO Anti-Dumping Agreement require that “the amount of the anti-dumping duty shall not exceed the margin of dumping or the margin of injury, whichever is lower.” Based on the injury data provided by Indian authorities, the 23%–30% duty rate is consistent with this principle.

2. Since 2022, India has imposed a 25% Basic Customs Duty (BCD) on PV products from China, and ALMM List-II (restricting government projects to using domestic cells) will be implemented in June 2026. The final ruling states that “anti-dumping duties and BCD serve different purposes and can be applied cumulatively,” so there is no need to push anti-dumping duties to a higher level.

3. Additionally, the low duty rate allows Chinese enterprises to comply without significant price increases, preventing a sharp rise in costs for downstream Indian power plant EPCs. This approach both supports the macro target of “280 GW of solar capacity by 2030” and reduces the risk of disputes at the WTO.

4. With 64.6 GW of new capacity concentrated in 2025–2026, the government only needs to provide protection until 2027 to achieve economies of scale. By then, lower costs will enable domestic producers to naturally compete against low-priced imports, eliminating the need for extended protection. Furthermore, ALMM List-II and the second and third tranches of the Production-Linked Incentive (PLI) scheme will take effect in 2026–2027. If anti-dumping duties are aligned, this could facilitate a smooth transition from tariff protection to subsidy support.

![[SMM PV News] CHN Energy Commissions 4 GW Lingwu PV Base on Subsidence Land](https://imgqn.smm.cn/usercenter/dtQDq20251217171740.jpg)

![[SMM PV News] France's 2025 Renewable Curtailment Doubles to 3 TWh](https://imgqn.smm.cn/usercenter/LlMgj20251217171739.jpg)

![[SMM PV News] Premier Energies Unveils India's First 0BB TOPCon Solar Cell](https://imgqn.smm.cn/usercenter/vghcI20251217171739.jpg)